Charles Hugh Smith

The dominoes of debt are toppling in Europe, and there is no way to stop the forces of financial gravity.

After 19 months of denial, propaganda and phony fixes, the political and finance leaders of the European Union are claiming a "comprehensive solution" will be presented by Wednesday, October 26-- or maybe by the G20 meeting on November 3, or maybe on Christmas, when Santa Claus delivers the gift global markets are demanding: a "solution" that actually pencils out and that forces monumental writeoffs of debt and thus equally monumental losses on European banks and bondholders.

There have been any number of insightful descriptions of what's going on beneath the artifice, spin and lies, for example:

Four Facts that PROVE the EFSF (rescue fund) Doesn’t Matter At All (Zero Hedge)

Revised Troika Forecast Sees Total Greek Debt-To-GDP Peaking At 186%: Here Is What Happens Next (Zero Hedge)

There Is No Bailout Spoon: The Math Behind The €2 Trillion EFSF Reveals A "Pea Shooter" Not A "Bazooka" (Zero Hedge)

Citi Expects A 76% Haircut On Greek Debt (Zero Hedge)

EU Bank Stress Test: When No. 1 Financial-Strength Ranking Spells Doom (Bloomberg)

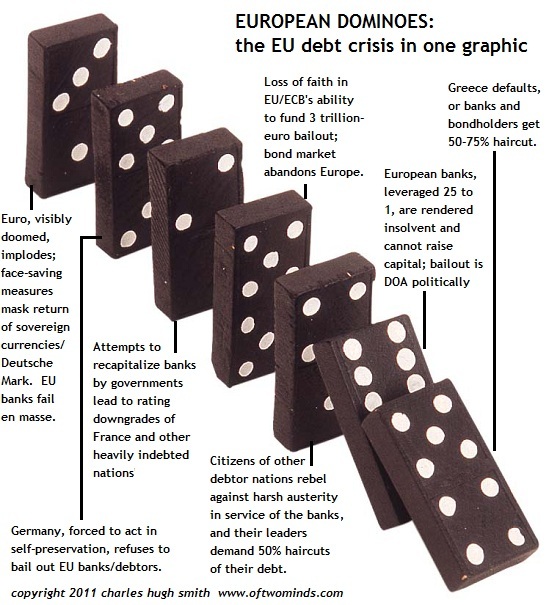

I have summarized the fundamentals in this one graphic: the European dominoes of debt. Simply put, there is no way the EU authorities can stop the first domino--Greek default or equivalent writedown of its impossible debt load--from toppling the over-leveraged banks which will be rendered insolvent when forced to recognize their losses.

That leaves each nation with the politically unsavory option of bailing out its premier banks with taxpayer money, and squeezing the money out of its citizenry via higher taxes and austerity. That assumption of bank debt will in turn trigger downgrades of heavily indebted sovereign nations such as France, moves that will raise rates and make the bailout even more costly to taxpayers, who will also be suffering from reductions of income due to global recession.

Once the banks and bondholders accept a 50%-75% writedown in Greek debt, then the other debtor nations will be justified in demanding the same writedown in their crushing debts. This dynamic leads to estimates that 3 trillion euros will be needed to bail all the players out. Alternatively, total losses will equal 3 trillion euros, wiping out banks and bondholders of sovereign debt.

The German economy is simply not big enough to fund a 3 trillion-euro bailout. Germany has 81 million people and its GDP is $3.3 trillion; the EU GDP is roughly $16 trillion. Compare those with the U.S., with 315 million people and a GDP of around $14.6 trillion.

As an act of self-preservation, Germany will be forced to either exit the euro outright or cloak its withdrawal with a "euro 1 and euro 2" scheme, a scenario I first laid out in March 2010: Why the Euro Might Devolve into Euro1 and Euro2 (March 2, 2010). (Other recent entries on the end-state of the European debt crisis:)

The Eurozone's Three Fatal Flaws (September 21, 2011)

The Dynamics of Doom: Why the Eurozone Fix Will Fail (July 25, 2011)

Why The European Union Is Doomed (March 28, 2011)

In any event, the last domino, the artifice of a single currency, will fall one way or another.

It's important to understand that the supposedly "prudent" economies of France, Germany, South Korea and Canada are just as heavily indebted as the U.S. or "drowning in debt" nations such as Italy. In the long view, is Germany's load of 284% of GDP really that different from Italy's 313%? Yes, the mix of debt is different, but the point is that all of Europe, and indeed the developed world, is overloaded with debt: state, bank and private.

The idea that leveraging more debt can resolve this gargantuan over-indebtedness is beyond absurd. (Source: BusinessWeek)

Read more here:

http://www.oftwominds.com/blogoct11/euro-debt-dominoes10-11.html

No comments:

Post a Comment